This has got to be one of the most practical and entertaining books I've gone through. It involves crazy smart mathematicians like Claude Shannon, John Kelly, Van Thorp working with gangsters like Longy Zwillman.

A few key concepts worth noting and still practical in today's markets,

1) Statistical arbitrage

Thorp started with Warrents (still traded over the ASX today), convertible bonds against underlying stocks. The average return of these guys in the 80s BEAT Warren Buffet's track record. There still exists plenty of other opportunities today.

2) The Kelly Criterion

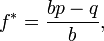

where:

- f* is the fraction of the current bankroll to wager;

- b is the net odds received on the wager (that is, odds are usually quoted as "b to 1")

- p is the probability of winning;

- q is the probability of losing, which is 1 − p.

3) Shannon's Demon

Claude Shannon was a freaking genius, and this is his version of a "balanced portfolio", where as long as the traded instrument IS indeed stochastic, a positive expectancy is guaranteed. So it can fit into the category of statistical arbitrage.

0 Reflections:

Post a Comment