"

The strategy gains its volatility overlay through the use of short-term VIX futures.

"

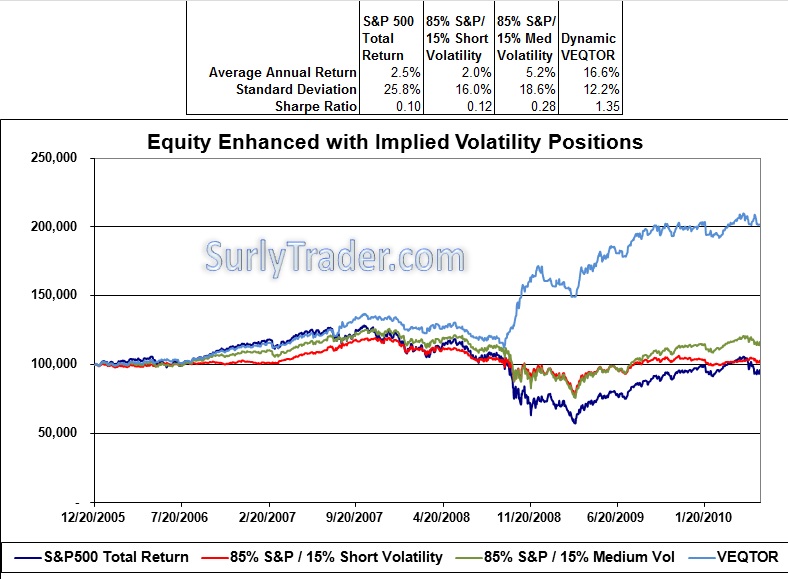

Basic idea here is to take a long position in VIX futures against equity holdings, rebalanced frequently with respect to expected future cross correlations. As a result, it theoretically offers a much smoother return and potentially make a net profit off volatility jumps like that of late 2008.

Performance of a Dynamic VEQTOR Strategy Allocation Algorithm against a naked long S&P500 position, (click on image to see the whole thing)

No comments:

Post a Comment